What is a Junior ISA account?

A Junior Individual Savings Account (Junior ISA or JISA) is a tax-free savings account for children under 18 who live in the UK. Introduced by the UK government in November 2011 to replace Child Trust Funds (CTFs), Junior ISAs allow parents, guardians and family members to save or invest tax-free on behalf of a child.

The key feature of Junior ISAs is their tax-free status. The interest on cash savings and the returns on investments in a Junior ISA are exempt from income tax and capital gains tax (CGT). This means more of your money can grow over time.

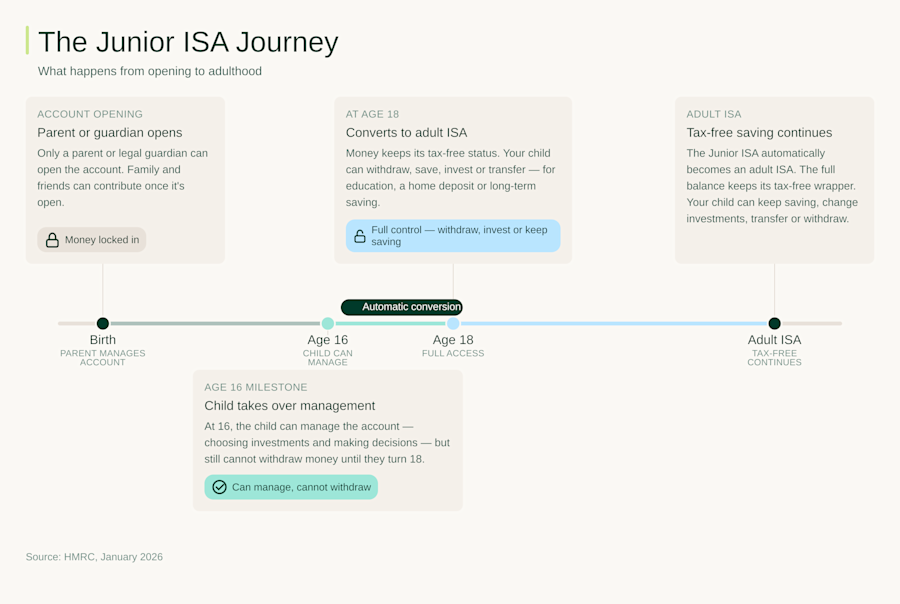

The money in a Junior ISA belongs to the child, but they cannot access it until age 18. At that point, the Junior ISA automatically turns into an adult ISA. The child, now an adult, can choose to carry on saving, invest a different way or withdraw the money.

Types of Junior ISA: Cash vs Stocks and Shares

There are two types of Junior ISA. They differ by risk and potential returns, as we explain below.

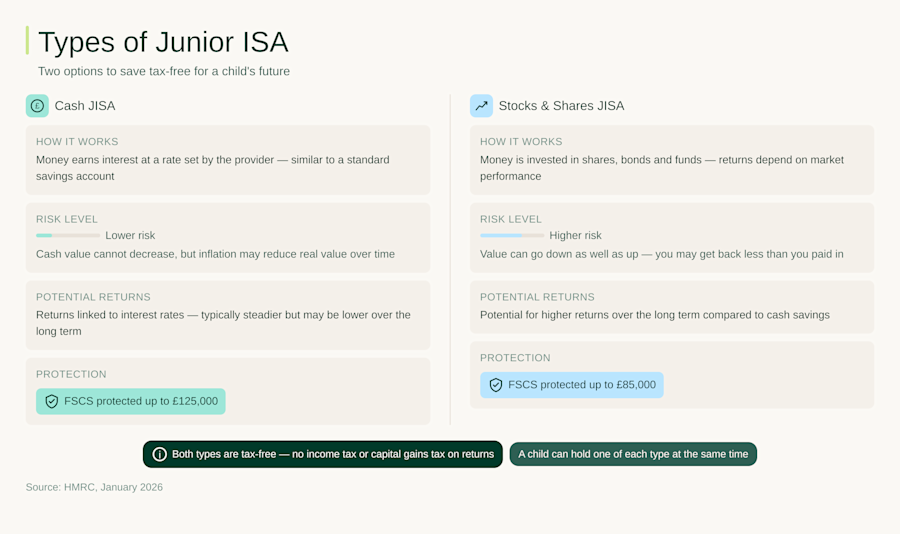

Cash Junior ISA

A Cash Junior ISA is like a standard savings account. The money you pay in earns interest. The provider sets the interest rate. This option is lower risk because the value of your cash cannot decrease. However, inflation can reduce the real value of your cash over time if interest rates do not keep up with rising prices.

If the provider is authorised by the Financial Conduct Authority (FCA), eligible deposits are protected by the Financial Services Compensation Scheme (FSCS) up to £120,000 per person, per authorised institution. This protection applies if the provider fails.

Stocks and Shares Junior ISA

A Stocks and Shares Junior ISA lets you invest in shares, bonds and funds. This option offers the potential for higher returns over the long term compared to cash savings. It also comes with more risk.

If the provider is authorised by the Financial Conduct Authority (FCA), eligible deposits are protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per person, per authorised institution. This protection applies if the provider fails. It does not cover investment losses.

Important: With a Stocks and Shares Junior ISA, the value of investments can go down as well as up. The child may get back less than you paid in. Past performance is not a reliable indicator of future returns.

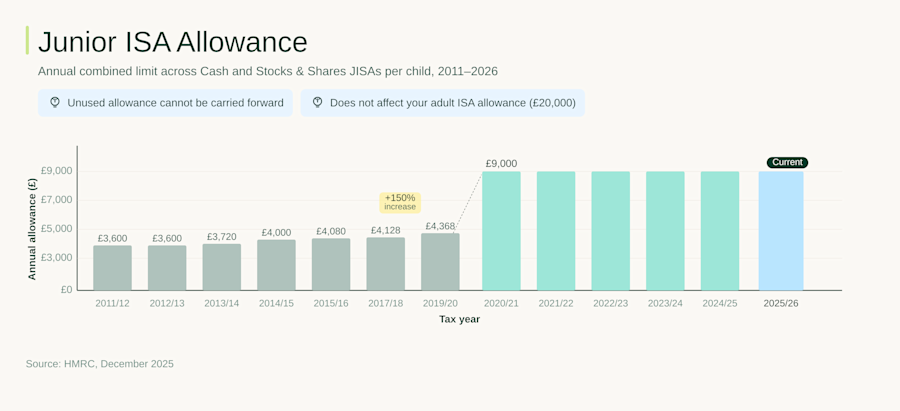

How much can you put in a Junior ISA?

The Junior ISA allowance for the 2025/26 tax year (6 April 2025 to 5 April 2026) is £9,000 per child. This is the maximum amount that you can pay in across all Junior ISA accounts per child, per tax year.

Key points about the Junior ISA allowance:

The £9,000 limit is a combined allowance for Cash and Stocks and Shares JISAs

You cannot carry unused allowance over to the next tax year

Contributions to a child’s JISA do not affect your own adult ISA allowance (£20,000)

Multiple people can contribute to the same child’s JISA

You must not pay in more than £9,000 in a tax year

Junior ISA allowance history

Tax Year | Annual allowance |

2011/12–2013/14 | £3,600-£3,720 |

2014/15–2016/17 | £4,000-£4,080 |

2017/18–2019/20 | £4,128-£4,368 |

2020/21–2025/26 | £9,000 |

Source: HMRC, December 2025

Who can open a Junior ISA?

Only a parent or legal guardian can open a Junior ISA for a child. The child must:

Be under 18

Live in the UK

Not have a CTF; if they do, you must convert it to a JISA

The person who opens the account becomes the registered contact. They manage the account until the child turns 16. At that age, the child can manage the account but still cannot withdraw money until 18.

Can grandparents open a Junior ISA?

No. Grandparents cannot open a Junior ISA for a grandchild. Under HMRC rules, only a parent or legal guardian can open the account. However, grandparents can pay into a JISA once the account is open.

Grandparents who want to contribute should:

Ask the parent or guardian to open a Junior ISA

Get the account details to pay money in

Check that total payments stay under the £9,000 yearly limit

Many providers allow grandparents, relatives and friends to pay money in by bank transfer or direct debit. Junior ISA contributions may count towards inheritance tax allowances, depending on the situation. Tax rules can change, so professional advice may be useful.

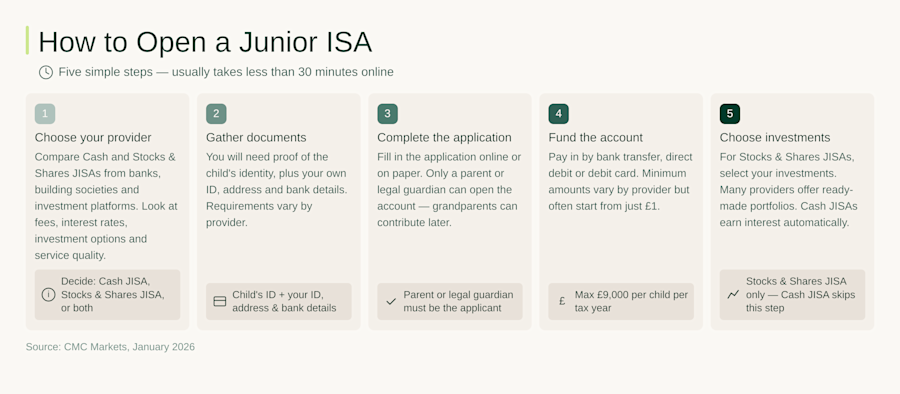

How to open a Junior ISA

Opening a Junior ISA is simple and usually takes less than 30 minutes online.

Here’s how it works:

Choose your provider and account type. Compare Cash and Stocks and Shares JISAs from banks, building societies and other providers. Look at fees, interest rates, investment options and service.

Gather documents. You will usually need proof of the child’s identity, plus your own ID, address and bank details.

Complete the application online or on paper.

Fund the account. You can pay in by bank transfer, direct debit or debit card. Minimum amounts vary by provider, but often start from £1.

If choosing a Stocks and Shares JISA, choose your investments. Ready-made options are often available, but may not suit your specific needs.

How many Junior ISAs can a child have?

A child can have up to two Junior ISAs at one time: a Cash JISA and a Stocks and Shares JISA. They cannot have more than one of the same type.

You can transfer a Junior ISA to another provider if you want better rates, lower fees or different investment choices. You must do the transfer through the new provider to keep the money tax-free.

Can you have more than one Junior ISA?

Yes, with limits. A child can hold one Cash JISA and one Stocks and Shares JISA at the same time. Total payments must not go above £9,000 a year.

This gives flexibility. For example, you could:

Split savings between cash and investments

Invest the full allowance for long-term growth

Keep all the money in cash if you prefer lower risk

What happens to a Junior ISA at 18?

When the child turns 18, the Junior ISA becomes an adult ISA. The money keeps its tax-free status.

At 16, the child can manage the account but cannot take money out

At 18, the account becomes an adult ISA. Your child (now an adult) can withdraw, save, invest or transfer the money.

He or she can use the money for any purpose, such as education, a home deposit or long-term saving.

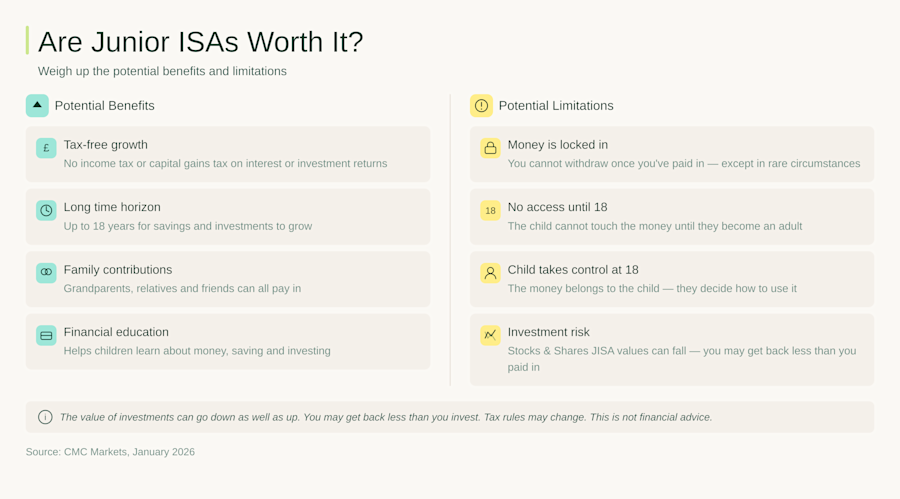

Are Junior ISAs worth it?

Junior ISAs can help build savings for a child. Whether they are right for you depends on your goals.

POTENTIAL BENEFITS | POTENTIAL LIMITATIONS |

|---|---|

Tax-free interest and investment growth | You cannot take money out after you have paid it in |

Long time to save and invest | Your child cannot access the money until age 18 |

Contributions from family members | The child controls the money at 18 |

Helps children learn about money | Investments can fall in value |

Important: The value of investments can go down as well as up. You may get back less than you invest. Tax rules may change.