Important: This information is for guidance purposes and may become out of date at any given time. It is not investment advice. Investments can rise and fall in value. We won’t make any assessment of whether the investments you chose are appropriate or suitable for you. If you are unsure of the suitability of any investment, investment service or strategy, you should seek independent financial advice. Capital is at risk.

You’ve probably heard it’s a good idea to have a diversified investment portfolio. And it is.

Building a diversified portfolio on your own, however, can be hard work. You’re required to research multiple securities and then assess whether these match your risk tolerance and investment objective when grouped together.

That’s why lots of investors choose to pool their money with other investors and utilise a mutual fund or ETF (exchange-traded fund) to gain exposure to multiple securities in a single trade.

The two vehicles have similarities, but also some key differences.

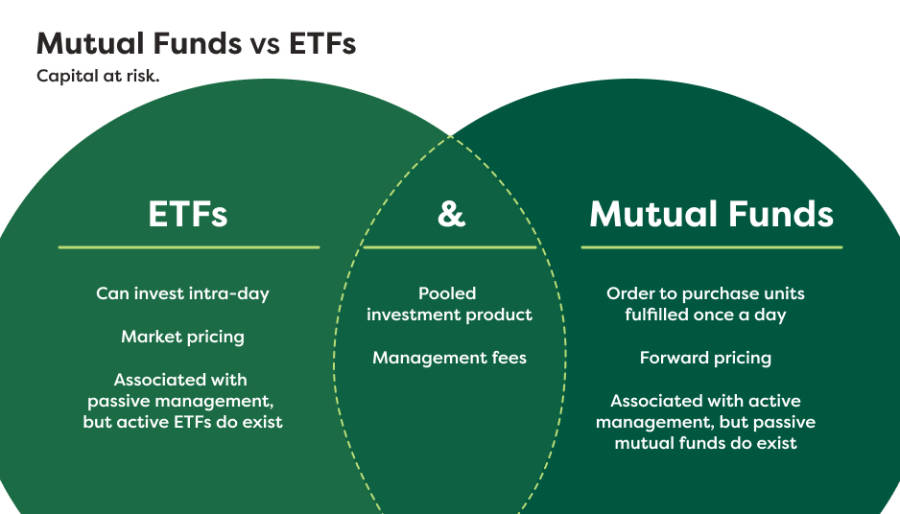

The two products have major similarities...

Before we get into the differences between these two products, let’s look at the similarities.

Both offerings involve pooling your money with other investors. This is then used to purchase assets based on the strategy of the mutual fund or ETF.

Let’s say you had £1,000 to invest. You could use this to purchase a handful of stocks yourself. Or, you could invest in one of these products and gain exposure to potentially hundreds of stocks or other assets.

With both products you’ll also pay a management fee – that’s the cost of all the admin involved in putting your money to work alongside that of other investors. This fee is normally a percentage of your investment. You can learn more about fees here.

Are ETFs easier to invest in than mutual funds?

One of the main differences between the two products involves how you invest in them. While some people will argue that ETFs are more straightforward in this regard than mutual funds, it largely comes down to personal preference.

When investing in an ETF you purchase shares that trade on exchanges. In the case of most UK-based investing platforms, this means purchasing shares that trade on the London Stock Exchange.

You can invest in an ETF, therefore, any time the exchange is open. As soon as you purchase shares, you’re invested, and you’ll know the price – which is based on the ETF’s underlying holdings – at which you purchased your stake.

This is also the case when selling out of an ETF. When selling shares in the product you’ll exit it immediately and know how much you’ve redeemed.

Mutual funds work slightly differently. To invest in them you purchase units created by the fund’s provider. These don’t trade on a stock exchange and, as a result, there isn’t continuous pricing throughout the day. Instead, the provider determines a price for the units once a day.

In practice, this means when you place an order to invest in a fund, you’ll purchase the units the next time their price is determined. This process is called forward pricing and it means that you won’t know the exact value of the units you’re buying when you place an order to invest. Likewise, when redeeming an investment in a mutual fund, you won’t know the exact amount you’re selling your units for.

A little active/passive misconception...

ETFs are mostly associated with passive management. This means they track the performance of an index – like the S&P 500 or FTSE 100. Their returns are determined by the movement of broader markets.

Many mutual funds are actively managed, meaning they have a portfolio manager making constant changes in a bid to help the fund meet its investment objectives. Managers could potentially identify assets that are set to outperform or counter market trends. This isn’t guaranteed, however, and past performance isn’t an indication of future returns.

Active funds normally come with higher fees – after all, you’re having to pay someone to continually keep an eye on a portfolio.

Some mutual funds, however, are passively managed. These are commonly referred to as “index” or “tracker” funds. They seek to replicate an index – like a passive ETF – but trade like a mutual fund. There is also a small, but growing, number of actively managed ETFs.

Are mutual funds really more expensive than ETFs?

Many mutual funds will require you to make a minimum investment in them. This could be a one-off lump sum each time you invest – say £100 – or it could be a smaller amount if you commit to investing regularly, on a monthly basis, for example. Minimum investments can vary from fund to fund and can also differ based on the investment platform you’re using.

An ETF doesn’t have a minimum investment per se. To invest you just have to purchase one share of the product. Again, this ranges from one ETF to the next. It could be a few pounds or a few hundred pounds.

While ETFs are also generally associated with lower fees than mutual funds, that doesn’t mean you’ll always pay less when investing in an ETF.

More niche ETFs – for example those focusing on a particular sector or theme – will have higher fees. Additionally, many low-cost index mutual funds have fees comparable to even the cheapest ETFs.

What’s right for me?

Investing is personal, so what works for one person won’t necessarily work for another.

Some investors favour the liquidity, transparency and (sometimes) lower fees associated with ETFs. Others gravitate to active mutual funds so that a portfolio manager can adapt to market conditions on their behalf.

When deciding, it’s important you research the strategy, objective and risk profile of the ETF or mutual fund you’re assessing. You should also check fees, which can eat into returns.

Ultimately, both products offer diversification in a single trade.