DBS will be issuing its business update for the third quarter of fiscal year 2024 (covering the period from October to December 2023) on 07 February 2024.

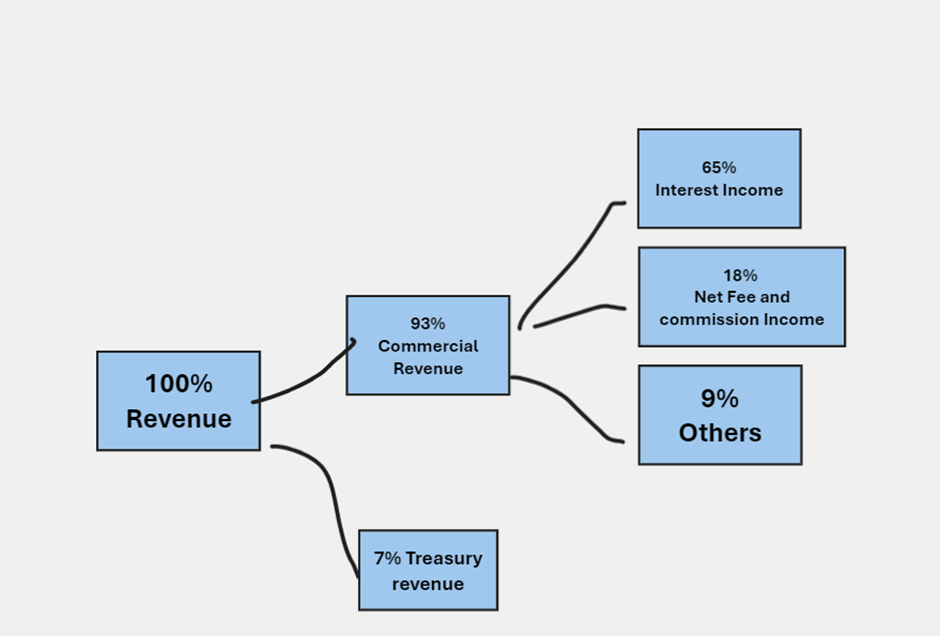

Over the past decade, the bank has demonstrated a consistent revenue pattern, with interest income accounting for approximately 55% to 65% of its total revenue. This trend underscores the bank's reliance on traditional banking operations, particularly interest from loans. A comprehensive examination of the bank's financials, as depicted in the accompanying chart, offers deeper insights into the factors shaping its revenue streams, notably interest rates, deposit amounts, and loan volumes.

Interest Income and Market Dynamics

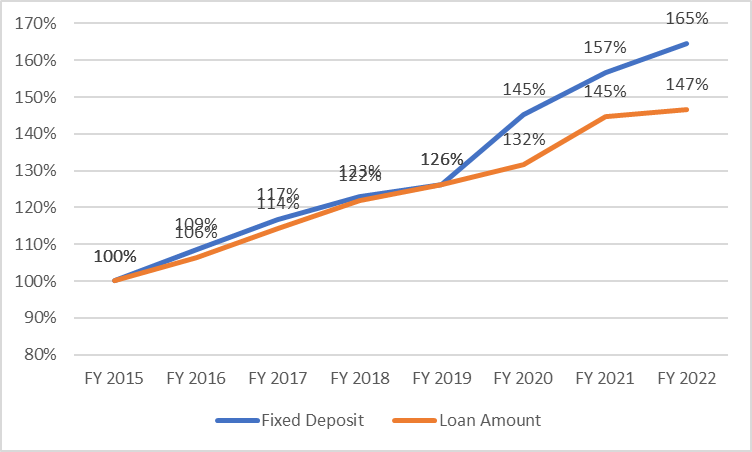

A critical factor influencing DBS's revenue composition is its interest income, directly affected by prevailing interest rates, deposit amounts, and loan disbursements. The provided chart, using FY 2015 as a baseline, indicates a relatively similar growth pattern for loans and deposits until FY2019-FY2020. However, a significant shift occurred during this period, where deposit values began outpacing loan amounts, primarily due to rising interest rates.

The surge in interest rates, escalating from 0.25% to around 4% since FY 2019, has resulted in a noticeable divergence. This divergence implies reduced revenue for the bank, as it now pays out more in interest due to faster growth in deposits relative to the growth of interest earned from loans. With the anticipation of sustained or increasing interest rates, this gap is expected to widen, potentially impacting the bank's profitability.

Property Market Slowdown and Its Implications

Another crucial factor to consider is the state of the property loan market. Recent data from Trading Economics reveals a significant slowdown in private home sales in 2023, reaching a decade low. This downturn is attributed to increased taxes and government restrictions. Given that property loans constitute a substantial portion of DBS's loan portfolio, this slump could further strain the bank's revenue growth.

Recent data from Trading Economics reveals a significant slowdown in private home sales in 2023, reaching a decade low. This downturn is attributed to increased taxes and government restrictions.

Outlook

In light of these market conditions, DBS Bank's growth prospects for the upcoming quarter appear constrained. The increased cost of deposit interest payouts, driven by higher interest rates, coupled with a sluggish property loan market, paints a challenging picture for the bank. This assessment aligns with forecasts from Investing.com, which predict a modest earnings per share (EPS) of 0.95 for the next quarter, a slight decrease from the previous figure of 1.01. Given the current financial landscape, this forecast seems realistic, leaving little room for an upward surprise.

The increased cost of deposit interest payouts, driven by higher interest rates, coupled with a sluggish property loan market, paints a challenging picture for the bank.

Technical Analysis

1. EMA indicators: Typically, when the shorter EMA crosses below a longer EMA, it's often considered a sign that the stock's short-term momentum is weakening relative to its medium-term trend.

2. RSI Trends: For DBS Bank, the RSI hitting 70 two weeks ago and currently trending downwards is significant. An RSI level of 70 or above typically suggests that a stock may be overbought, potentially leading to a pullback or reversal. The subsequent downward trend in RSI can be seen as confirming this bearish momentum.

3. $30.50 is the next support level.

In conclusion, DBS Bank faces challenges in maintaining robust revenue growth amid a complex financial landscape characterised by rising interest rates and a slowdown in the property loan market. While technical indicators point towards a bearish outlook, forecasts indicate a modest earnings decrease for the next quarter. As the bank navigates these challenges, strategic adjustments may be necessary to sustain its financial performance in the ever-evolving market conditions.

This article is for educational purposes and not to be regarded as investment advice, a recommendation, or an offer or solicitation to subscribe for, buy or sell any investment product. All forms of investments are subject to risks, including the possible loss of the principal amount invested. Losses can exceed your initial deposit. You should carefully consider your investment experience and objectives, financial situation, and risk tolerance level, and consult an independent financial adviser prior to dealing in any investment products. The contents in the article may have been obtained or derived from public or other sources believed by CMC Invest to be reliable. However, unless otherwise specifically stated, CMC Invest makes no representation as to the accuracy or completeness of such sources or the information, and accordingly accepts no liability for loss whatsoever arising from or in connection with the use of or reliance on the information. Please visit www.cmcinvest.com/en-sg/ for important information. This article has not been reviewed by the Monetary Authority of Singapore.

such articles? Stay up-to-date with regular market insights and analysis, investing tips and more, delivered directly to your inbox.

Invest with transparency today

Invest with transparency today