SG Special – When Will Singapore Stocks Start Performing?

Aug 18, 2024 | CMC InvestSingapore stocks are boring. What will it take to shake things up?

The prevailing sentiment is that Singapore's stock market suffers from poor valuations and low liquidity. Key challenges include a lack of new listings, frequent delistings, and a limited base of retail investors. Suggestions for revitalising the market include listing government-linked companies, allowing pension and sovereign funds to invest locally, and supporting high-growth firms.

Singapore stocks are good paymasters, but there have been no windfalls yet

Source: Weipedia

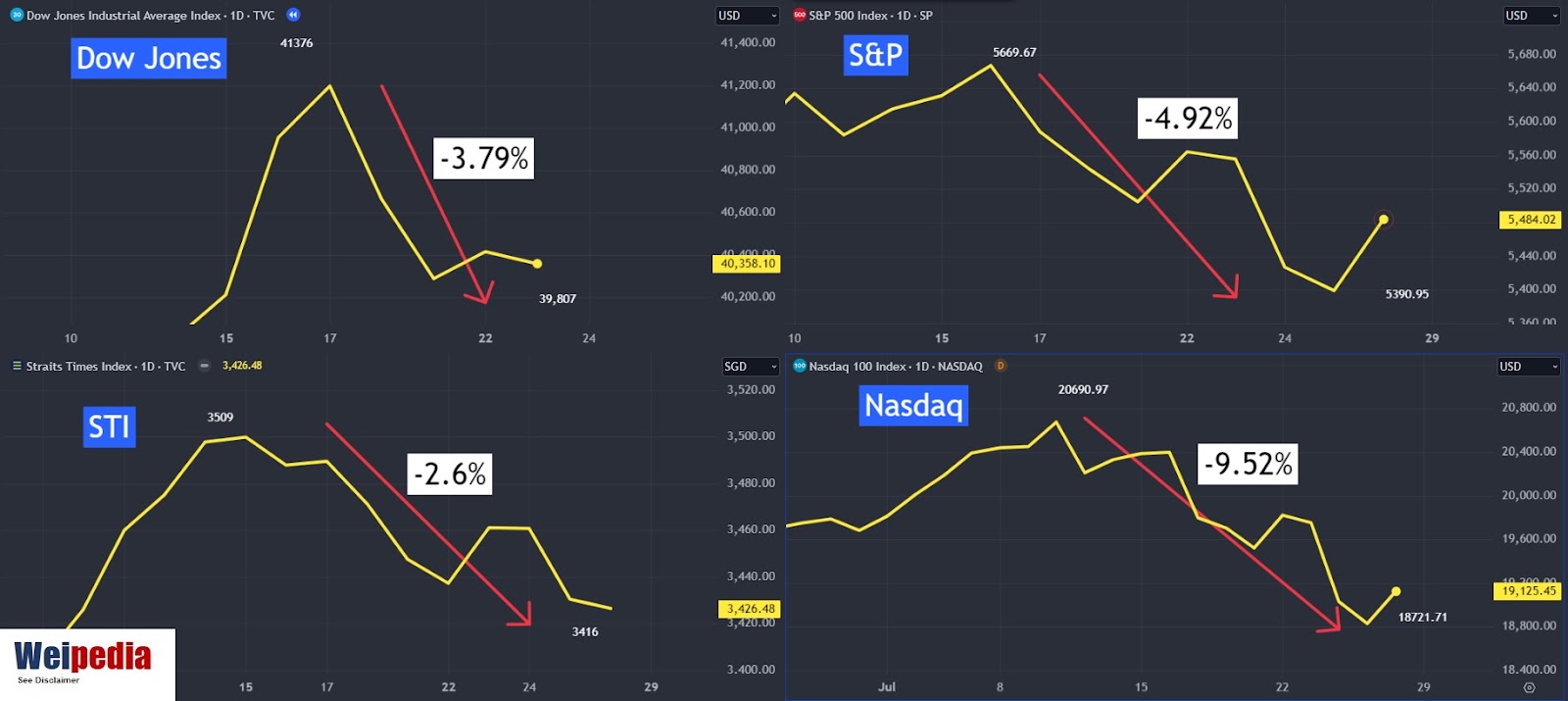

Despite these challenges, Singapore stocks have consistently offered generous dividend payouts, especially when compared to technology services or finance sectors in NYSE and SGX. However, the downside of dividend stocks is that their strategy of returning earnings to shareholders may explain the range seen in the following chart:

Source: TradingView

A strategy for dividend investors to consider is investing at market lows during a crisis and taking profits during market hype. Over the last 20 years, there have been five cycles. This approach allows investors to benefit from both dividends and capital gains.

“A strategy for dividend investors to consider is investing at market lows during a crisis and taking profits during market hype.”

However, this requires skill and time in managing these market cycles. For those who prefer to be passive dividend investors, we need to look at returns in totality. The STI Total Return Index provides a good gauge, as shown in the following chart, as it accounts for both capital gains and the reinvestment of dividends. Since the STI Total Return Index launched on 11 April 2022, to their recent high, the STI increased by 39%, whereas the STI Total Return Index increased by 123%.

Source: TradingView

Demand for safe haven asset is greater than before

According to UNCTAD's World Investment Report 2023, Foreign Direct Investment (FDI) inflows to Singapore reached a record-high of USD 141.2 billion in 2022, up from USD 131.1 billion one year earlier (+7.7%), making the country the third-largest FDI recipient worldwide after the U.S. and China, and accounting for almost two-thirds of flows to ASEAN countries. In June 2022, US inflation reached a peak of 9%, and global stock markets were down for the entire year. Yet, Singapore achieved record FDI. This clearly signals that during times of crisis, global investors view Singapore as a safe haven.

The next crisis may not be bad for Singapore stocks

Could it be AI fatigue or another inflation fear? Although the latest inflation rate has eased to 3%, any escalation of geopolitical risks could quickly cause inflation to climb back up, resulting in market turmoil. Technically, the STI has been trying to breach the 3,400 level since 2007. However, if it can close above 3,400 in the coming quarters with a high inflow of investment, this would indicate a psychological breakthrough.

Source: TradingView

My investing strategy

As the debate continues about allowing pension and sovereign funds to invest locally, we should consider examples from other countries, such as the United States, Australia, Japan, and Malaysia, which have regulations to recycle a large part of their domestic savings – be it pension or retirement savings plans – and insurance monies back into their domestic markets. Supporting our local markets may provide some stability, but the key is to continue grooming and creating a value proposition for our listed companies to attract global investors.

There is a chance of flight to quality from the West to the East among global investors in the next crisis. Regarding my strategies, I will continue to accumulate value stocks with attractive dividend payouts and add more when the momentum starts after convincingly breaking above 3,400.

This article is for educational purposes and not to be regarded as investment advice, a recommendation, or an offer or solicitation to subscribe for, buy or sell any investment product. All forms of investments are subject to risks, including the possible loss of the principal amount invested. Losses can exceed your initial deposit. You should carefully consider your investment experience and objectives, financial situation, and risk tolerance level, and consult an independent financial adviser prior to dealing in any investment products. The contents in the article may have been obtained or derived from public or other sources believed by CMC Invest to be reliable. However, unless otherwise specifically stated, CMC Invest makes no representation as to the accuracy or completeness of such sources or the information, and accordingly accepts no liability for loss whatsoever arising from or in connection with the use of or reliance on the information. Please visit www.cmcinvest.com/en-sg/ for important information. This article has not been reviewed by the Monetary Authority of Singapore.

such articles? Stay up-to-date with regular market insights and analysis, investing tips and more, delivered directly to your inbox.

Invest with transparency today

Invest with transparency today