Self-invested Personal Pension

With our Premium plan, you can invest towards your retirement with our tax-efficient, flat-fee, SIPP (in partnership with Quai Investment Services Ltd). You’ll also have access to all the benefits that come with both our Core and Plus plans, which means you'll get a General Investment Account and access to a Flexible Stocks and Shares ISA.

When you invest, your capital is at risk. Tax treatment depends on your individual circumstances and may change in future. Access your pension money from age 55 (57 from 2028).

Transfer bonus

Earn up to £1,000* when you transfer a minimum of £25,000 into any of our CMC Invest accounts. Just use our seamless, in-app transfer request. *T&Cs apply.

Why invest with us?

Premium for £0*

That’s right! You can enjoy our Premium plan for £0 a month for 12 months*. All you have to do is download the app, create an account and switch to our Premium plan. *T&Cs apply.

£0 commission

Have more cash to put towards your investments by saving money on commission on every trade. Other charges apply.

More flexibility on drawdowns

Choose the best way to use your pension with our drawdown options. You'll have the option to take out your tax-free lump sum in smaller amounts from the age of 55 (57 from 2028) until you’ve reached your overall 25% tax-free allotment.

Variety of investments

Invest in 3,000+ US shares, Large-cap UK shares, 400+ ETFs, Investment Trusts and REITs. With Plus, you’ll get Mid and Small-cap UK shares, AIM shares and 1,000+ Mutual Funds. See our price plans for more information.

Earn 2% interest

You will earn 2% gross interest (2.02% AER) on your uninvested, settled cash within your SIPP account. Read more about our 2% cash interest here.

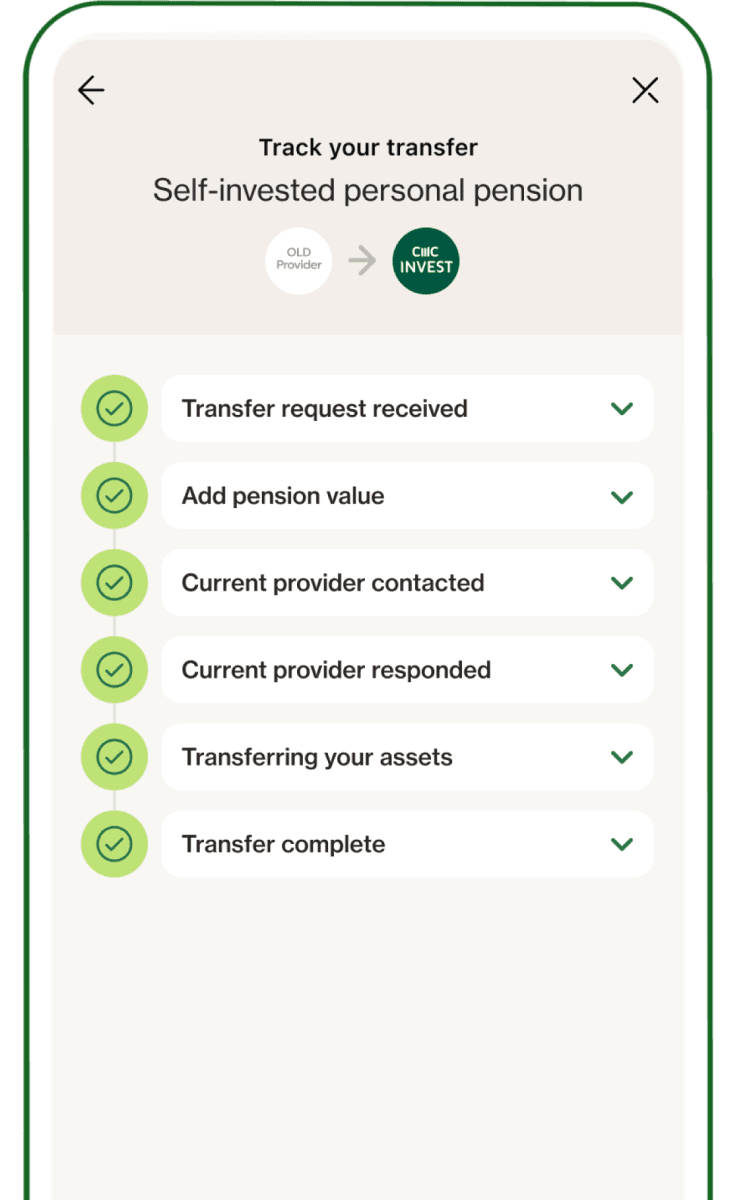

In-app transfers

Combine and manage your old pensions with our easy-to-use in-app transfer form and start a transfer request in as little as 30 seconds. Learn more about our transfer process.

What is a SIPP

A Self-invested Personal Pension (SIPP) allows you to take control of your retirement and to have the choice on what, when and how much you invest. This could be a great option to save and invest towards your dream retirement in a tax-efficient way that puts you firmly in charge.

A SIPP has the same tax benefits as a traditional pension, which means you can get tax relief (based on your marginal tax rate), on your personal contributions up to the annual allowance. But it's important to remember that a SIPP works like a normal pension, so you won't usually be able to get money out until the age of 55 (rising to 57 from 2028). You can contribute to a SIPP alongside other pensions, like a workplace pension.

Tax treatment depends on your individual circumstances and may change in future.

Have more flexibility with your drawdown

When you want to take your 25% tax-free lump sum, many pension providers require you to do that all-in-one go, but if you don’t need it all-in-one go, why take it? We give you more flexibility by allowing you to take out smaller amounts gradually until you reach your 25% tax-free allotment.

Do you have more questions about a SIPP? Check out our FAQs

SIPP guidance

We’re with you on your financial journey, visit the learn hub to find out more about investing.

Straightforward and transparent price plans

Browse and choose from one of our plans that suits what you need. No hidden fees, no nasty surprises, just straightforward and transparent pricing. FX fees and UK government charges may apply.

Core

Plus

Premium

Core plan

£0

Always pay nothing for our Core plan. Our Core plan will always be £0/month.

Accounts

- General Investment Account

- Flexible Stocks & Shares ISA

- Self-invested Personal Pension

Benefits

- £0 Commission

- 3,000+ US shares

- Large-cap UK shares

- 400+ ETFs and Investment Trusts

- 2% interest on cash balances

OFFER

Plus plan

£10 £0

Get our Plus plan for £0/month for the first 3 months* then pay up to £10/month.

Accounts

- General Investment Account

- Flexible Stocks & Shares ISA

- Self-invested Personal Pension

Benefits

- Everything in Core

- 1,000+ Mutual Funds

- Mid & Small-cap UK shares

- AIM shares

- USD & EUR wallets (GIA only)

OFFER

Premium plan

£25 £0

Get our Premium plan for £0/month for 12 months^, then pay up to £25/month.

Accounts

- General Investment Account

- Flexible Stocks & Shares ISA

- Self-invested Personal Pension

Benefits

- Everything in Core and Plus

When you invest, your capital is at risk.

*Plus plan 3-month free promotion terms and conditions.

^Premium plan 12-month free promotion terms and conditions.

For the full list of platform benefits, compare our price plans.

Frequently asked questions

How does the tax-free lump sum work?

Let’s say you retire at 65 with £500,000 in your pension and you need £20,000 to pay off the final part of your mortgage. To do this, you carve out an £80,000 portion of your pension and withdraw 25% of this, which is £20,000. The remaining £60,000 is set aside as taxable income that still has a chance to grow.

Can you repeat this process as many times as you like for different amounts until you’ve reached your overall 25% allotment, which in this case would be £125,000.

Who is a SIPP best suited to?

SIPPs are best suited to people who have some investment experience, the time and knowledge to apply that experience, and the confidence to manage their own longer-term retirement finances. While SIPPs are ‘self-invested’, you may want some support from an independent financial adviser.

If you’re considering transferring old pensions, it’s best to first check you won’t lose any benefits, and whether there are any exit fees.

What tax relief are pensions eligible for?

When you pay into a pension you qualify for tax relief on those contributions. The amount you get depends on your tax rate. As a basic-rate UK taxpayer, you’ll receive tax relief at the same rate, but the way it works can seem a bit confusing at first, so here’s a straightforward example:

Let’s say you want to add £100 to your pension. To do this, you pay in £80 and the government adds £20 as tax relief. Your pension scheme claims this from the government, so effectively, you get a 25% tax credit.

If you pay higher-rate income tax (40%), you can claim up to a further 20% in tax relief through your annual self-assessment tax return. This is paid to you (or reduces your tax bill) rather than to your pension, and you could then pay this tax refund into your pension. The same applies for additional-rate (45%) taxpayers, who can claim back a further 25%.

Scotland has different tax rates to the rest of the UK, so If you’re a Scottish taxpayer the amount of tax relief you can claim is different, but the process works in the same way.

Tax rates and rules can change over time, and the relief you receive depends on your personal circumstances.

How much tax relief can I get on pension contributions?

There’s no limit to how much you can pay into your pensions in any one tax year, but there is a limit to how much you’ll receive tax relief on. You can pay in up to 100% of your annual earnings or £60,000, whichever is the lower, and get tax relief. This limit is known as the ’annual allowance’ and is set by the government.

Higher earners have a reduced annual allowance, known as the ‘tapered annual allowance’. This applies once your earnings exceed £200,000 and your ‘adjusted income’ exceeds £260,000. It means your annual allowance decreases by £1 for every £2 you earn above £260,000. The minimum tapered annual allowance is £10,000 and this kicks in once your adjusted income reaches £360,000.

If you don’t have any taxed income you, or someone else, can still pay-in your pension and get tax-relief. The amount contributed is limited to £2,880 which, together with the basic rate tax relief totals £3,600.

If you haven’t used your full annual allowance in any tax year, you can carry forward the unused part from up to the previous three years. In the tax year you want to use that carry forward part, you must have used all your annual allowance and then have sufficient ‘relevant UK earnings’ to cover the carry forward amount too.

How do I contribute to my CMC Invest SIPP?

Contributions are made via the CMC Invest app using your registered debit card. Simply log in, tap on the SIPP account from the home page and then on the ‘Add cash’ link.

Can I transfer other pensions to my SIPP?

Yes, you can. Most types of pensions can be transferred to your CMC Invest SIPP, including pensions you’ve already taken benefits from.

If you’re thinking about transferring a current workplace pension, please make sure your employer will continue to make contributions to your SIPP, otherwise you would be deemed to have ‘opted-out’ of the workplace scheme and those contributions would be lost. You should also check that the pensions you’re thinking of transferring don’t have any benefits (like the right to access them early, or enhanced benefits) that could be lost when transferring.

‘Defined benefit’ workplace schemes are not as common as they used to be, but if you do have one, or a pension with ‘safeguarded benefits’, you would lose those when you transfer. This is generally not considered to be in your best interests, so you are required to get financial advice from an authorised firm confirming a pension transfer is recommended for you before we can accept it.

Can I transfer my CMC Invest SIPP to another pension scheme?

Yes, you can. We don’t charge any exit, transfer, or closure fees. You’ll first need to set up your new pension with your chosen provider and tell them you want to transfer your SIPP from us to them. Your new provider will then contact us and arrange the transfer.

It may be that assets held in your CMC Invest SIPP can’t be held by your new provider, in which case you’ll need to sell them before the transfer can be completed.

If you’re looking to transfer your SIPP to an overseas pension scheme, we’ll need to ensure the scheme is recognised as an eligible scheme to transfer to. Transferring to a scheme that’s not a recognised overseas pension scheme could result in you incurring a significant tax charge. We therefore recommend that, when considering such a transfer, you seek independent financial advice from a firm authorised to advise on pension transfers.

Once the transfer is complete, your CMC Invest SIPP account will be closed. Any other accounts you hold with us won’t be affected and you should then switch from our Premium plan to the Core or Plus plan.

Can I take my pension earlier than age 55?

In most cases, you can’t access your pension early. This is because the government has set the normal minimum pension age at 55. However, you may be able to do so if you are diagnosed with a serious ill-health condition, typically meaning you have less than 12 months to live.

Some pension schemes used to have a protected pension age lower than 55. This typically would have been removed before 2006 though, and usually only applied to sportspeople and entertainers, where their career meant that they retired at an earlier age. However, this doesn’t apply to SIPPs. If you have a lower protected pension age with a pension you’re considering transferring to a SIPP or another personal pension, you would lose this benefit when transferring.

The state pension age for men and women is currently 66 for those born between 6 April 1954 and 5 April 1960. This is the earliest you can take your state pension, but you can choose to defer taking it until a later date and then get an uplift in your pension when you do. The state pension age is due to rise to 67 in 2028.

Is there a limit on how much I can build up in a pension?

From 6 April 2024, the Lifetime Allowance (LTA) disappears and is replaced by three new allowances.

The Lump Sum Allowance (LSA) limits the tax-free cash you can take from your pension to a maximum of £268,275.

The Lump Sum and Death Benefit Allowance (LSDBA) is the limit on tax-free withdrawals from your pension you can get in your lifetime via a Serious Ill Health Lump Sum and when you die. This is set at £1,073,100.

If you have taken tax-free cash from a pension before 6 April 2024, your previously used LTA percentage will be converted into a reduction in both the LSA and LSBDA. If you exceed the LSA or the LSDBA, the excess will be taxed at your marginal rate.

The other new allowance is the Overseas Transfer Allowance (OTA) for those transferring their pension abroad. This is set at £1,073,100.

If you have previously taken benefits from your pension, transferred your pension overseas or have reached age 75 and not received 25% of your previously used Lifetime Allowance as tax-free cash, you may be able to apply for a Transitional Tax-Free Certificate.

Further information can be found by visiting the Money Advice Services website.

Who provides the CMC Invest SIPP?

Whilst CMC Invest provides investment and execution services, we are not an investment advisor or a regulated pension provider. We’ve teamed up with Quai Investment Services Limited, who are an experienced pensions and SIPP provider. Quai provides the underlying pension service while CMC Invest provides the mobile app and account for managing your SIPP, and the investments within it.

CMC Invest is not a pensions operator or administrator, nor does it provide investment advice. Individual investors should make their own decisions or seek independent financial advice. The value of investments can go up as well as down and you may receive back less than your original investment. CMC Invest is a trading name of CMC Markets Investments Ltd, which is authorised and regulated by the Financial Conduct Authority (948126). Registered in England and Wales. Company number: 12816952. Quai Investment Services Limited acts as a pensions operator and administrator and is authorised and regulated by the Financial Conduct Authority (922590). Registered in England No 09919243, VAT No 401610949. The Registered Office for Quai Investment Services Limited is Unit 16 Tesla Court, Innovation Way, Peterborough, PE2 6FL.

Scan the QR code to install the app

App Store

Play Store

- 01Scan the QR code with your mobile phone's camera

- 02Download the app from your app store

- 03Follow the in-app instructions to create an account in minutes

When you invest, your capital is at risk.